The Loan Officer Accountability Scorecard: Track What Actually Matters

Most loan officers track the wrong thing. They obsess over closed loans — a lagging indicator that tells you about decisions made 45 to 90 days ago. By the time a bad week shows up in your closings, it's already too late to course-correct.

A real loan officer accountability scorecard tracks the inputs that create closings. It tells you today whether next month is going to be strong or weak. And that early warning system is the difference between a managed business and a business that's managing you.

Why Most Accountability Approaches Fail

The word "accountability" triggers eye-rolls from a lot of experienced loan officers. They've been in "accountability groups" that amounted to sharing numbers in a Facebook group twice a month with zero consequence for missing targets. They've had managers who reviewed pipelines but never challenged the activity generating those pipelines.

That's not accountability. That's theater.

Real accountability coaching for mortgage professionals isn't about shame or pressure — it's about clarity. When you have a weekly scorecard with five specific metrics, you know exactly where your business is healthy and where it's leaking. The conversation becomes surgical, not motivational. "Your new conversations were at 8 last week, down from 15 the week before — what happened Tuesday?" That's a coaching conversation worth having.

The goal of a scorecard isn't to judge performance. It's to surface the patterns that separate a $150K producer from a $400K producer.

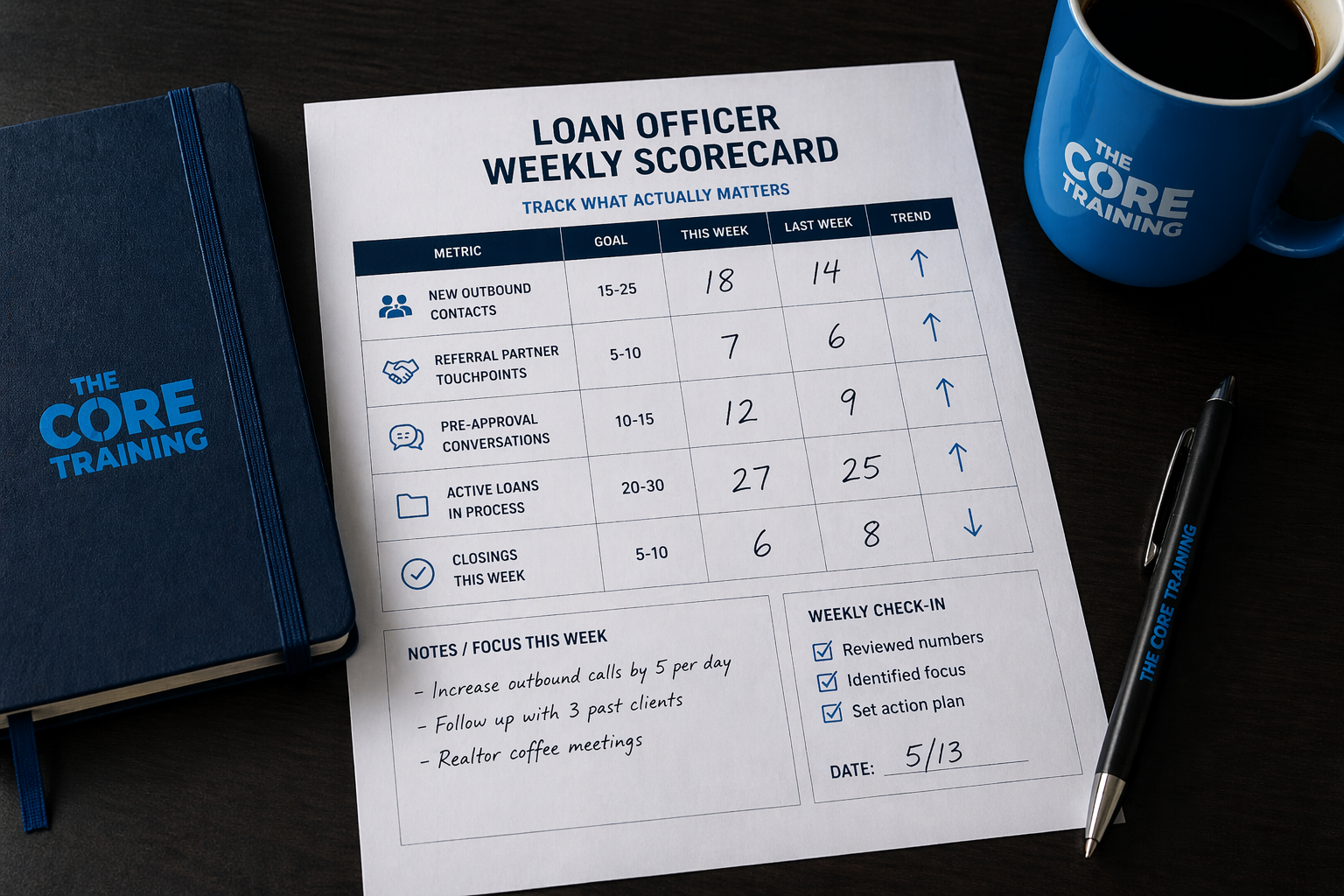

The Five Metrics Every Loan Officer Scorecard Needs

Every effective weekly scorecard for mortgage production tracks three leading indicators, one concurrent indicator, and one lagging indicator.

Leading Indicators (predict future business):

· New outbound contacts made: Raw conversations started this week with potential borrowers or referral sources. Goal: 15–25 per week.

· Real estate agent/referral partner touchpoints: Quality contacts with active or prospective referral partners. Goal: 5–10 per week.

· Pre-approval conversations initiated: Borrowers moved from lead to active engagement.

Concurrent Indicator (current pipeline health):

· Active loans in process: Every loan currently moving through your pipeline, with a projected close date.

Lagging Indicator (historical output):

· Closings this week: The result of decisions made 45–90 days ago. Don't manage to this number alone — but track it to validate that your inputs are converting.

Five metrics. Fifteen minutes on Monday morning. That's your scorecard.

How to Make Yourself Accountable When You Work Alone

For independent or small-team loan officers, accountability is harder to manufacture. There's no manager watching. No team meeting. Just you and your calendar.

Here's what works:

Anchor accountability to a ritual, not a person. Pick one time each week — Monday at 8 AM, or Friday at 4 PM — to review your five scorecard numbers. Make it as non-negotiable as a closing.

Create consequence by publishing your numbers. Not publicly, necessarily — but to someone who will ask about them. A colleague. A peer in a coaching group. A partner.

Set a rolling 4-week view. Don't just look at this week. Look at the trend over four weeks. Are your leading indicators rising, flat, or declining? A single bad week is noise. A three-week decline is a signal.

Scorecards Work Only If You Take the Numbers Seriously

The most common failure mode with accountability scorecards isn't inconsistency — it's rationalization. "I only made 8 contacts because we had a company meeting." Every excuse sounds reasonable in isolation. But every excuse compounds.

The scorecard's job is to create a clear, honest picture of your activity. Your job is to look at that picture without flinching. When the numbers are down, something specific happened — and that something is usually inside your control to change.

High-producing loan officers aren't immune to bad weeks. They're better at diagnosing them and correcting faster.

What THE CORE Members Do Differently

Inside the Locker Room — The CORE's $250/month community with a 7-day free trial (thecoretraining.com/locker-room) — members review their scorecards in a structured weekly format alongside other producers. The shared accountability isn't social pressure; it's pattern recognition. When 40 loan officers are reviewing the same five metrics every week, the group gets very good at spotting what separates a high-output week from a low one.

Rick Ruby built The CORE scorecard framework from years of watching what actually moved the needle for producers at every volume level. It's not theoretical — it's the framework he and his members use to run their own businesses.

If you're going to finish the year on your terms, start tracking the right inputs today. The scorecard is free. The results are on you.

Join the Locker Room and get The CORE weekly scorecard template used by members across the country. Start your free 7-day trial. → thecoretraining.com/locker-room

share this

Related Articles

Related Articles